Why Legacy Banking Systems Struggle With Digital Transformation

It’s very much a case of survival of the fittest in the digital banking and fintech sectors right now. Adapt or die! Digital transformation is now non-negotiable for legacy providers looking for long-term survival.

But the bigger the platform, the harder the path to modernization becomes. Despite pouring millions into digital transformation planning and software development, legacy systems are proving highly resistant to change.

Many of the issues are structural. And no amount of resources can solve the problem without a fit-for-purpose plan of action. That’s where a digital transformation consultant can prove invaluable — along with an experienced software development team.

Let’s take a close look at the reasons behind the inability of legacy banking systems drive home digital transformation strategies.

Let’s Address the Elephant in the Room: Monolithic Architecture

Let’s head back to the start of the fintech revolution. Those first banking apps seemed revolutionary at the time. And they were. But they were built with monolithic architecture. Single, tightly-coupled codebases were largely developed for maximum reliability and batch processing when people were still restricted to banking on desktop computers.

Monolithic architecture raises a number of issues for developers. Every component is intertwined with all the others. Making the tiniest of changes to one of these components can significantly affect all the others. Before you know it, that simple change requires a comprehensive reworking of the entire platform. That’s expensive and time-consuming.

Did you know that 90% of banking software in the US is considered legacy ? This means that some of the world’s biggest financial institutions are struggling to deliver their digital transformation plans.

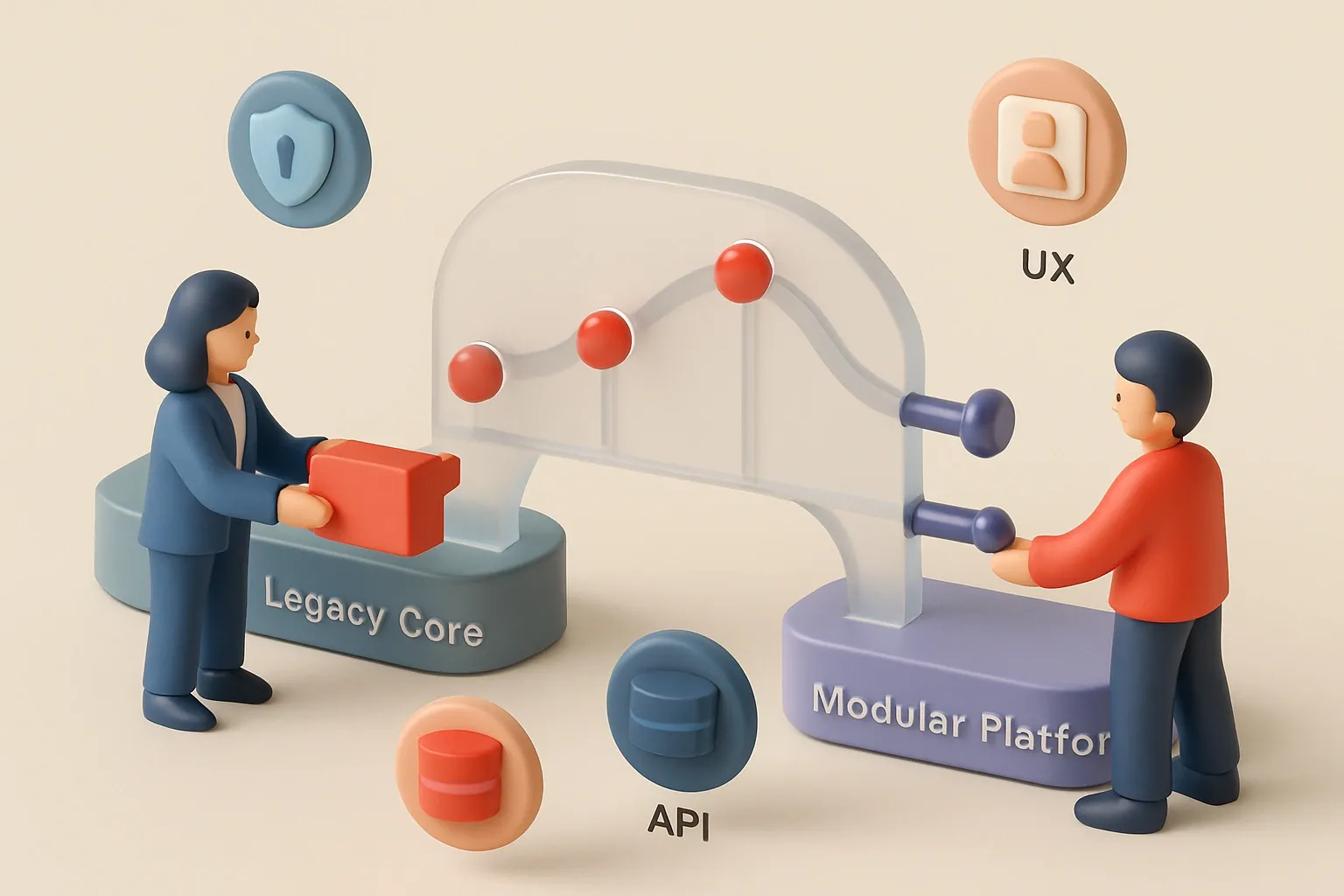

But there’s some good news: Modular architecture can be modified and updated faster and more cheaply. It involves a series of microservices, which means independent components communicate with each other via APIs. These systems allow teams to update, scale, and replace individual services while leaving the rest untouched.

Lots of banking platforms still rely on outdated monolithic architecture, however. It’s just easier. Or at least that’s the perception. And the longer the spaghetti of interwoven components grows, the harder (and more expensive) it becomes to modernize.

The Danger of Half Measures When It Comes to Digital Transformations

Digital transformations for banks and banking platforms are notoriously complex, expensive, and time-consuming. That’s why many institutions opt for partial strategies. They replace a select few subsystems but leave the core untouched. But there are some serious issues with partial digital transformations:

- Escalating maintenance costs for aging mainframes and outdated languages

- Persistent data silos that prevent real-time insights

- Missed market opportunities due to prolonged product launch cycles (while fintech competitors move in weeks)

When there is so much at stake for legacy banking institutions, it’s easy to understand why so many choose this half measure. But in reality, they get the worst of both worlds. The costs of development are still high, while the new capabilities remain limited.

Why Frontend Fixes Don’t Work

Take it from us, there are no quick fixes or shortcuts when it comes to successful digital transformations in the banking sector. We know because we’ve seen many institutions attempt to refresh the customer-facing components of their applications while leaving the core system intact. Yes, the refreshed application might look great. It may, initially, feel revolutionary. But it’s never long before the cracks begin to appear.

- Batch processing delays

- Limited API capabilities

- Data inconsistencies

You may get some good feedback on frontend changes, at first. But over time, customers may start reporting issues such as transfer delays, incomplete account reports, and tricky customer journeys.

This is when the costs start to spiral. Even frontend changes are expensive and time-consuming to implement. But because customers need more help, support costs also creep upwards. Those customers eventually become frustrated, and they either engage less or simply look elsewhere.

And there’s evidence to suggest that limiting digital transformations for banks to frontend modernization causes backend bottlenecks, limits digital progress, and restricts real-time capabilities. Remember: A shiny paint job doesn’t turn an old banger into a supercar. Sometimes, it’s best to strip everything down and start from the beginning.

The Outcome-Based Approach to Digital Transformation Sets the Stage for Success

In our experience at DigiNeat, the outcome-based approach to digital transformation delivers the best results. While every case has its own challenges, the following steps pave the way for future-proof banking platforms:

- Define measurable business outcomes

- Adopt progressive modernization — step by step, rather than giant leaps

- Form cross-functional teams that own the entire process

- Measure progress against business results

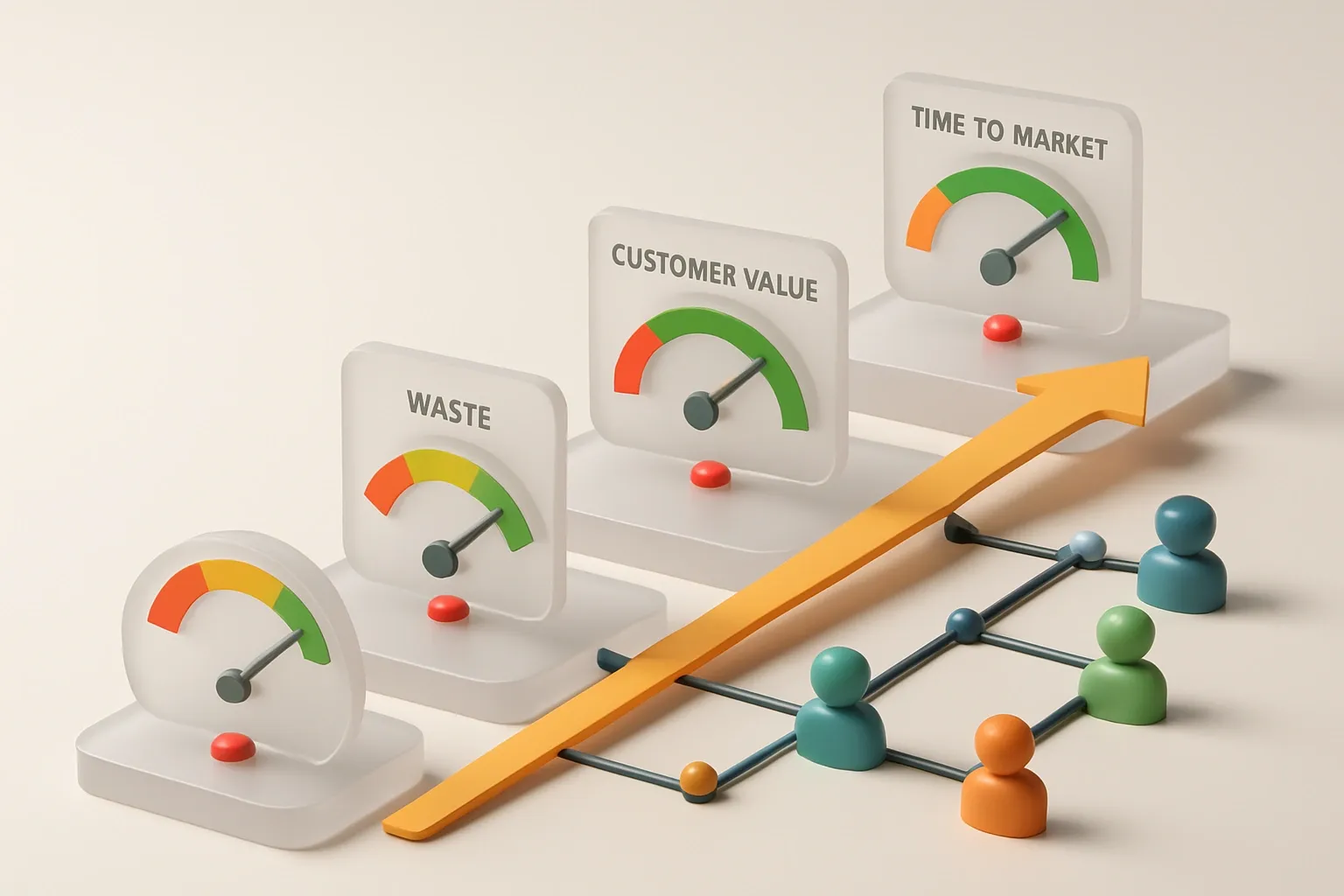

Banking institutions that complete successful digital transformations — mostly with outcome-based approaches — achieve time-to-market improvements of around 60%.

The race is on to modernize legacy platforms in the banking industry. That’s why so many institutions want a definitive roadmap, an immovable timeline, and a fixed budget. They’re taking the “big bang” approach, rather than embarking on a sustainable journey with plenty of pit stops along the way.

We’ve seen it time and time again. Outcome-focused software and app development delivers a range of benefits that banking institutions find invaluable:

- Delivers real customer value, not just features

- Reduces waste and unnecessary work

- Brings teams in line with business goals

- Increases team motivation and purpose

- Enables faster learning and quick pivots

- Improves resource efficiency and ROI

- Creates a stronger overall business impact

Partner with Proven Software Developers for a Smoother, More Successful Transition

The legacy infrastructure that is currently holding back banking platforms is real and complex, but there are solutions. The move towards modular architecture, avoiding superficial, frontend fixes, and focusing on business outcomes, is making a difference. And that’s why we’re making these three strategies central to our digital transformation planning.

Ready to move beyond the limitations of legacy banking systems? Contact the DigiNeat team today for a free strategy session.